Congress is officially set to move forward with legislation that will alter the retirement saving landscape once again, more than a year after passing landmark legislation that rattled Americans in and near retirement as well as their retirement savings plans. Coined as the SECURE Act 2.0, the House Ways and Means Committee unanimously approved a markup of the legislation to be sent to the House floor for a full vote before it makes its way to the Senate Chambers. The legislation’s official title is,

Securing a Strong Retirement Act of 2021 and it looks to advance on much of the progress that was included in the original SECURE Act.

The original SECURE Act, titled Setting Every Community Up for Retirement Enhancement Act, was passed in December of 2019, and was signed into law by former President Donald Trump. At the time of its passing, the legislation was one of the biggest retirement reforms in recent years eliminating the stretch-IRA, raising the required minimum distribution age, and eliminating the age limit for retirement plan contributions, among other items. The new legislation looks to expand on some of these provisions such as increasing the required minimum distribution (RMD) age again, but incrementally over the next ten years.

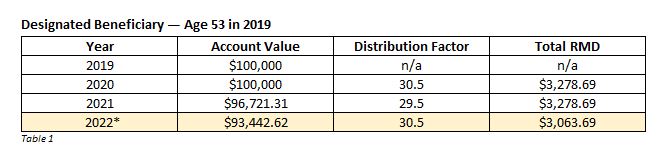

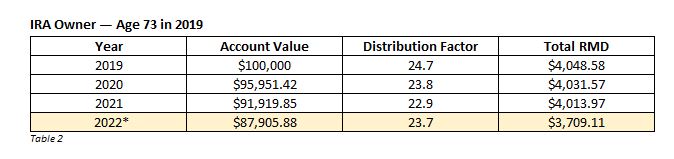

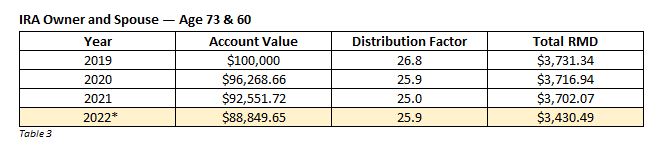

By raising the RMD age, retirees will have more time to allow their accounts to grow before being mandated to make withdrawals. Prior to 2020, the RMD age was 70 and a half years old which was then raised to 72 in the first SECURE Act. Should the SECURE Act 2.0 pass through Congress and be signed into law by President Biden, the RMD age would immediately increase to 73 as of January 1, 2022. According to the current language of the proposed legislation, it would then take several more years for the RMD age to rise to age 74 on January 1, 2029, and then finally reaching 75 on January 1, 2032. If this legislation does become law, individuals who are 63 or younger in 2021 would be able to delay their RMDs to age 75 once the full increase is in place.

Ultimately, by raising the RMD age investors who have money in traditional IRA vehicles will have more time (if their age qualifies) to increase the total amount of their investment by not having to take withdrawals. Even just a few extra years can help a retiree build their nest egg, especially since traditional IRA accounts are tax deferred. The potential issues that could arise from these incremental increases is confusion among retirees about when to take their RMDs and making sure that they do so correctly to avoid penalties for withdrawing too early or late or simply not accepting their required payments because they have no guidance of when they should take them. If these provisions are rolled out for the public, it will be important for investors to ensure that they are receiving the proper advice to handle their retirement investments and take full advantage of the age increase.

Another important update in the proposed SECURE Act 2.0 is increasing the catch-up contribution which gives older workers over the age of 50 the ability to invest more money, above the limits set by the Internal Revenue Service (IRS), to bolster their nest egg in the years before they reach retirement. The additional benefit of making a catch-up contribution is that investors will also be lowering the amount of taxable income for that tax year, ultimately reducing the amount of money owed to the IRS. As of January 1, 2021, the catch-up contributions set by the IRS are $1,000 for IRA accounts, $6,500 for traditional 401(k) and other workplace retirement plans, and $3,000 for SIMPLE retirement plans. What legislators hope to achieve with the SECURE Act 2.0 is to raise those contribution limits from $6,500 to $10,000 starting at age 62 through 64 and from $3,000 to $5,000 for SIMPLE plans. The legislation would keep current contribution limits starting at age 50 with the additional increases coming into effect starting at age 62.

Legislators have stated that these proposed increases will also be indexed for inflation and will go into effect starting in 2023. It is unclear whether the additional increases will remain after age 65, or if the contribution limits will revert to the original contribution limits for individuals over the age of 50. Now, the language of the proposed legislation seems to indicate that the increases for catch-up contributions will only impact those who have reached the ages of 62 through 64 to provide a few brief years of extra support to strengthen their retirement nest egg.

The SECURE Act 2.0 legislation also looks to expand access to 401(k) plans by setting up automatic enrollment for employees in new company plans along with other provisions dealing with matched contributions to assist with student loan repayments. Currently, the language of this bill is subject to change as it was first sent to the House of Representatives on May 5, 2021 and must go through more legislative channels before it can finally be sent to the Senate and eventually to President Biden’s desk for signature. Proponents of this legislation are confident that the bill will be passed with overwhelming bipartisan support in the Congress, but with the current state of domestic political affairs, bipartisanship is never a given, especially with policy decisions involving economic issues.

Two of the foundational aspects of the SECURE Act 2.0 deals with the raising of the RMD age and the three-year period where investors will be able to contribute exponentially more in terms of a catch-up contribution. This combination will enable retirement investors to grow their nest egg for a longer period than previously allowed which may lessen some of the retirement strain that many Americans have and are currently experiencing. Delaying the RMD age to 75 over the next ten years will create larger income payments for retirees in tandem with their Social Security benefits and any other investments that they may have.

Sponsors of the legislation also anticipate that the SECURE Act 2.0 will help generate more than $27 billion in tax revenues over the next ten years. It is important to remember however that if this legislation is signed into law, individuals already receiving RMDs from their investments will continue as the provisions in the bill are not retroactive to include those who already had their RMDs delayed to age 72. If this legislation does become law, retirees and those nearing retirement should make sure they get educated about the changes that will directly impact their retirement goals to ensure their retirement strategy still aligns with their best interest and to take advantage of boosting their savings if applicable when the time comes.